The maritime industry stands at a turning point in 2025. As international shipping faces increasing regulatory and market pressure to decarbonize, wind propulsion has re-emerged, not as a nostalgic nod to the age of sail, but as a cutting-edge technology delivering measurable efficiency gains. With momentum growing, the coming years will be decisive in shaping how wind propulsion helps the industry achieve the International Maritime Organization’s (IMO) ambitious goal of net-zero greenhouse gas emissions by 2050.

A decade ago, wind propulsion was still viewed as experimental and interesting technology but far from mainstream. Trials with Flettner rotors, rigid wings, suction wings, and even large kites generated curiosity, but uptake was limited and many in the industry remained skeptical. High upfront costs, uncertainty in regulatory recognition, and limited operational data meant that projects were often dismissed.

However, several forces converged to change this perception. Rising fuel costs and volatile markets made efficiency a commercial necessity. At the same time, the urgency of decarbonization and the tightening of international regulations, starting with the Energy Efficiency Design Index (EEDI) and later the EEXI and CII, created a new framework where technologies like wind propulsion could no longer be ignored. Technological advances in automation, materials, and design also made systems more reliable, more cost-effective, and easier to integrate into large ocean-going vessels.

By the mid-2020s, what was once seen as unlikely had crossed the line into commercial reality. Wind propulsion is no longer a demonstration technology but a scalable, proven contributor to efficiency and emissions reduction, setting the stage for the industry-wide uptake we are now witnessing.

As of early 2025, there are 81 large vessels either operating with wind propulsion systems (71) or classified as wind-ready (10). These installations span a broad range of vessel types: bulk carriers and tankers dominate (22 each), followed by general cargo ships (19), RoRos (10), and smaller shares across ferries, containerships, and specialist vessels. This diversity demonstrates that wind technologies are no longer confined to niche experiments but are adaptable across the global fleet.

Momentum is accelerating quickly. More than 130 additional vessels are under construction, on order, or undergoing retrofits, with the majority expected to be delivered during 2025–26. In total, these represent over 4 million dwt of shipping capacity already equipped with wind propulsion, plus nearly 400,000 dwt classified as wind-ready. This is not an incremental trend, it is a transformational shift in how ships are designed, built, and operated. For the first time since the age of sail, the wind is returning to the center of maritime propulsion—this time backed by technology, regulation, and market demand.

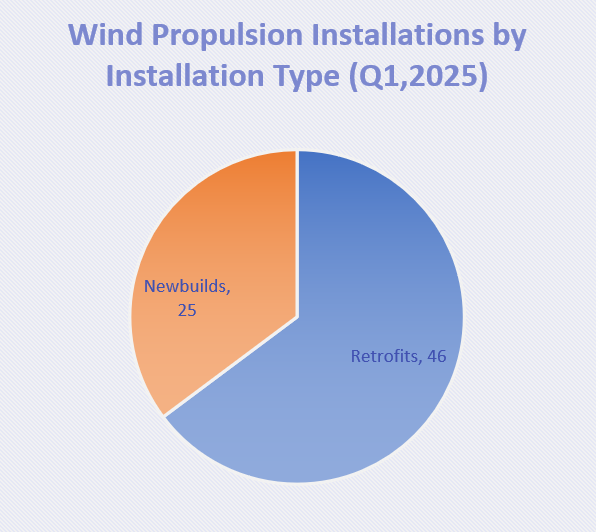

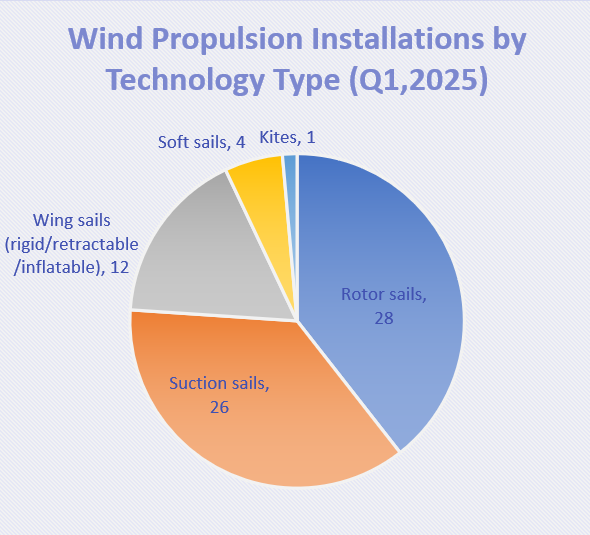

Looking only at the 71 vessels already in operation with wind propulsion systems, two patterns stand out. On the installation side, the majority are retrofits (65%), reflecting how owners have so far chosen to adapt existing vessels. However, the share of newbuilds (35%) is rising as shipyards begin to design vessels with wind propulsion to maximize their performance. On the technology side, the market is dominated equally by rotor sails (39%) and suction sails (37%), which together make up more than three quarters of all installations. Wing sails (17%) are emerging as a third option, particularly on larger bulkers and tankers, while soft sails (6%) and kites (1%) remain niche but demonstrate the diversity of solutions under deployment.

(Vessel List – Wind Propulsion Installation List)

It is important to note, however, that today’s distribution of technologies reflects more the influence of installation costs, technology maturity, and the availability of providers over the past few years than a final verdict on which solutions are best. There are still many unknowns, such as which technologies perform most effectively on different vessel types, in varying operational profiles, or across specific trading routes. As the market expands and more data is collected from real-world operations, these shares are expected to shift significantly. What we see today is a snapshot shaped by early market dynamics; over time, the relative weight of each technology will adjust as experience grows, performance evidence accumulates, and shipowners gain a clearer view of the most effective system for each segment and route.

Forecasts show that adoption is set to expand sharply by 2030, with EU studies projecting up to 10,700 installed systems across global fleets. Tankers and bulk carriers will lead the way, with wind-assisted fleets scaling from just a few hundred vessels today into the thousands within a decade.

By 2050, the UK government projects that up to 40,000 vessels, representing 40–45% of the world fleet could incorporate wind propulsion technologies. At that point, wind will not be a retrofit option but an integral part of vessel design and operations, standing alongside new fuels and efficiency measures as a cornerstone of decarbonization.

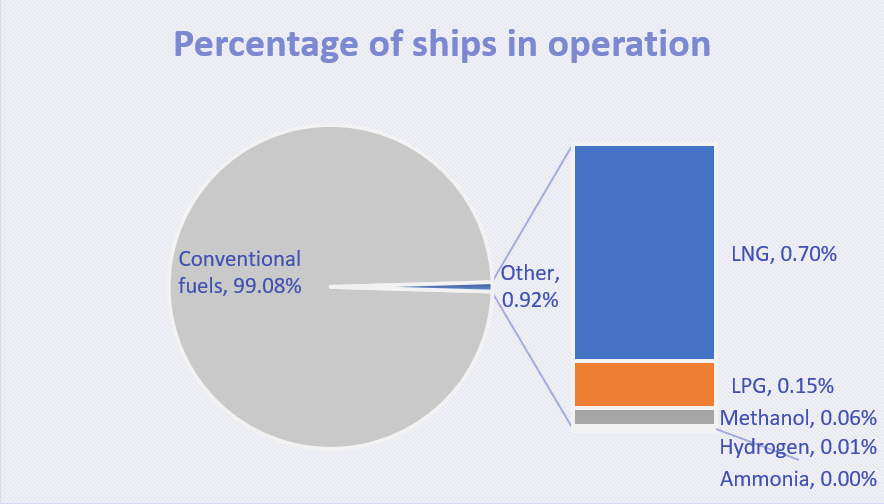

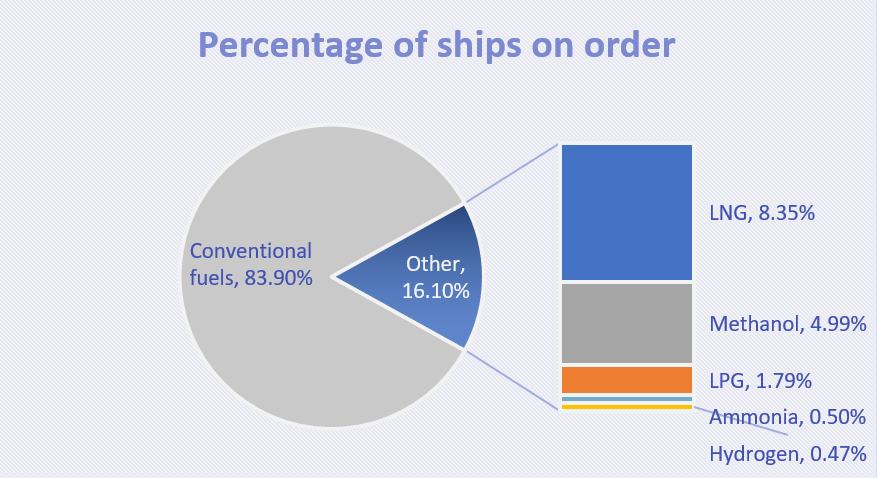

The broader energy transition reinforces this trajectory. According to DNV data, the uptake of alternative fuels (LNG, LPG, methanol, hydrogen, and ammonia) is increasing year after year. Yet, in the 2050 decarbonization scenario, wind propulsion is positioned as one of the largest global markets for emission reduction technologies, with a projected annual market potential of £1,900–2,100 million.

What sets wind apart is its fuel-agnostic nature: regardless of whether ships transition to methanol, ammonia, or hydrogen, wind propulsion consistently reduces fuel demand, lowering costs and emissions simultaneously.

In recent years, the IMO has made energy efficiency the cornerstone of shipping’s decarbonization strategy. IMO has started to adopt a holistic, energy-focused approach to decarbonization, moving beyond a narrow, fuel-only view. This shift acknowledges that technologies like wind propulsion, which directly reduce energy demand, must be properly integrated into regulatory mechanisms if the sector is to achieve its 2030, 2040, and 2050 decarbonization checkpoints.

Early measures such as the Energy Efficiency Design Index (EEDI) for newbuilds and the Energy Efficiency Existing Ship Index (EEXI) for the operational fleet have already pushed shipowners to adopt design improvements and retrofit solutions. Complementing these, the Carbon Intensity Indicator (CII) came into force in 2023, requiring operators to track and report their emissions intensity, with Phase II tightening requirements from 2024 onward.

Crucially, wind propulsion is now being integrated into this regulatory framework. The IMO, in close collaboration with the International Towing Tank Conference (ITTC) and other technical bodies, is advancing methods to properly account for wind as a renewable energy source. This includes the development of standardized performance assessment protocols, ensuring that wind-assisted ship propulsion (WASP) systems are recognized in EEDI/EEXI and CII calculations.

At the same time, regulation is increasingly tied to market-based incentives. From 2025 onwards, mechanisms such as FuelEU Maritime and forthcoming IMO market-based measures will apply a penalty/reward system linked to vessel CO₂ intensity. Ships that outperform efficiency thresholds, through the integration of solutions such as wind propulsion, will benefit from reduced compliance costs, while those falling behind will face mounting penalties.

For a long time, many decarbonization assessments underestimated, or even excluded, the contribution of wind propulsion. This began to change with MEPC.1/Circ.896 (2021), which provided guidance on how innovative energy efficiency technologies, including wind, could be accounted for in EEDI and EEXI calculations (IMO Circular). The recognition gained further weight with MEPC 79/INF.21, a submission by Comoros, RINA, IWSA and several other member states, which highlighted the underestimated potential of wind and called for fairer treatment in IMO strategies (MEPC 79/INF.21 submission).

At MEPC 82 (2024), a new proposal outlined a tiered methodology (MEPC 82/7/9) for measuring wind propulsion’s contribution within the Attained GHG Fuel Intensity (GFI) formula. This framework offers different levels of precision, from simplified analytic models to detailed ship-specific trials and direct thrust measurements, ensuring wind systems can be credited fairly while allowing methodologies to improve as more operational data becomes available (IWSA submission).

At MEPC 83 (April 2025), the IMO approved the draft Net Zero Framework, which combines a goal-based fuel standard with economic measures such as carbon pricing. This framework is expected to embed methodologies for crediting wind propulsion within future amendments to MARPOL Annex VI (IMO summary). At the same time, the terms of reference for the Fifth IMO GHG Study have been expanded to explicitly assess all energy sources, including wind propulsion, on an equal footing with alternative fuels (IWSA paper).

These policy shifts are tied to a clear set of regulatory milestones, each one raising the ambition:

Together, these developments mark a turning point, wind propulsion is no longer an overlooked technology but a recognized energy source within the IMO’s regulatory structure. Embedding it into efficiency indices, GFI formulas, and future market-based measures ensures that its contribution is fairly acknowledged.

This evolving framework is doing more than setting limits; it is reshaping the economics of shipping. Wind propulsion delivers direct and immediate CO₂ reductions today, with fuel savings typically ranging between 5–35%, depending on vessel type, system configuration, and route.

Recent sea trials confirm these figures: Bound4Blue’s eSAIL® system, installed on the Ville de Bordeaux (Louis Dreyfus Armateurs, chartered by Airbus), achieved average daily savings of 1.7 tonnes of fuel, peaking at 5.4 tonnes per day, avoiding over 2,181 tonnes of CO₂ annually (Well-to-Wake) (Bound4Blue, 2025). Meanwhile, the Canopée, fitted with four OceanWings® units, has delivered 1.3 tonnes of daily fuel savings per wing, with recent transatlantic voyages recording 2.2 tonnes per wing per day and even achieving 13.7 knots under sail power alone (OceanWings, 2025).

While the exact level of savings depends on factors such as the type of vessel, the number and arrangement of wind propulsion systems, and the trading routes they operate on, they provide real-world proof points that wind propulsion is no longer a concept but an operationally reliable, commercially relevant solution. The fact that these savings are being recorded under today’s conditions explains why adoption is accelerating, especially as new market-based measures amplify the financial benefits of early action.

If 2025 marks the tipping point, the decade ahead will decide whether wind propulsion remains a niche efficiency tool or becomes a mainstream pillar of maritime decarbonization. With over 4 million dwt of wind-propelled capacity already sailing and hundreds more vessels in the pipeline, the foundation has been laid.

By combining wind propulsion with alternative fuels, route optimization, and new vessel design, the maritime industry can accelerate toward the IMO’s net-zero vision. And in this transition, WASP systems are not just supplementary, they are essential.

Wind propulsion has evolved from “nice to have” into a strategic necessity. The numbers already prove the case: dozens of vessels in operation, hundreds more on the way, and millions of tons of shipping capacity already cutting fuel use and emissions. The journey to 2050 will be long and challenging, but one thing is clear: without the wind, shipping’s path to net zero will be much harder, and far more costly to sail.